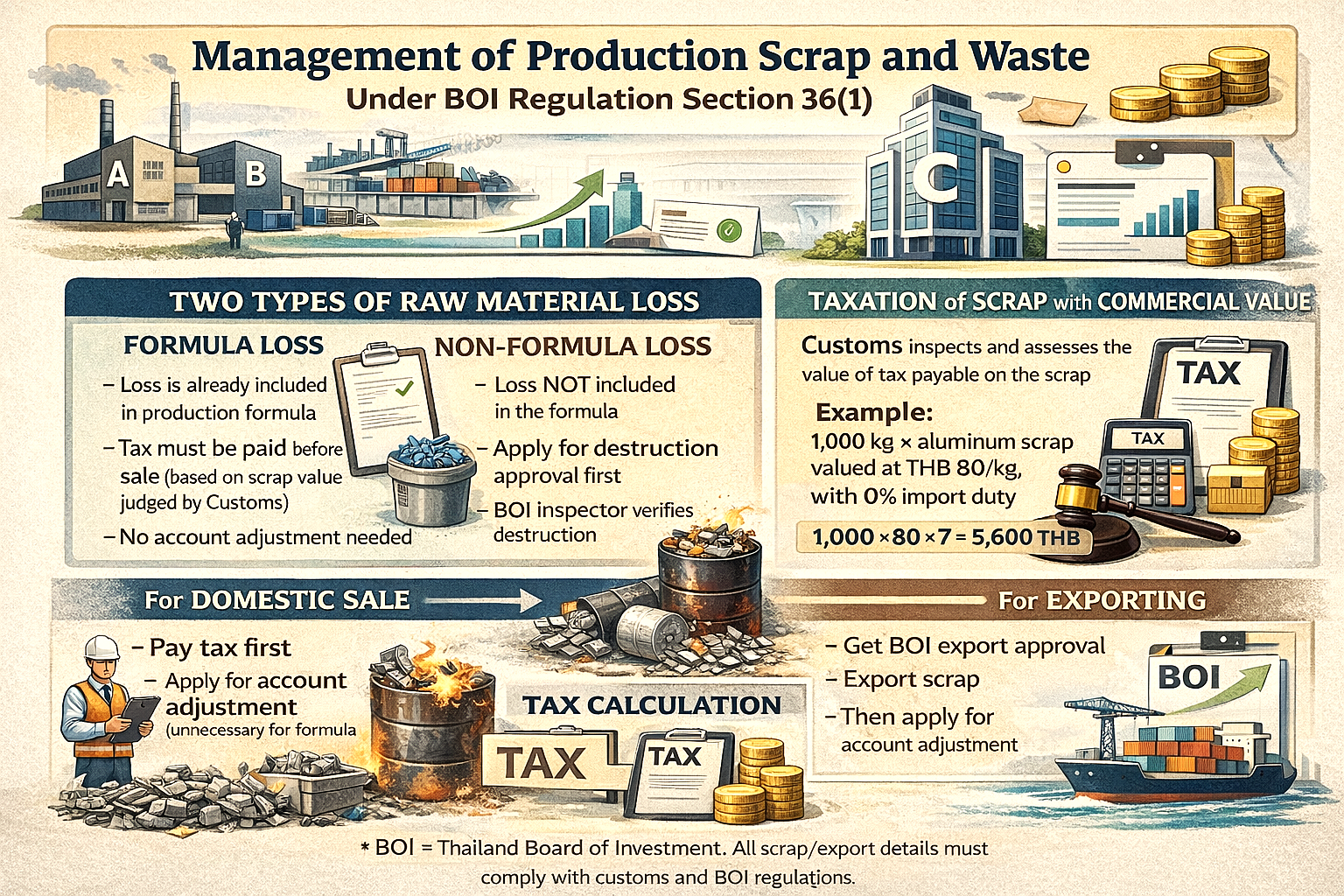

Raw material loss is divided into two types:

- Loss Included in the Production Formula (Formula Loss)

- Loss Not Included in the Production Formula (Non-Formula Loss)

1. Loss Included in the Production Formula (Formula Loss)

- The loss quantity is already included in the approved production formula.

- No separate account adjustment is required because the loss is automatically deducted together with product clearance via customs declaration or Report-V.

- However, since the scrap remains in Thailand, if it has commercial value, it must either:

- Be exported, or

- Be sold domestically after paying tax based on the condition of the scrap.

2. Loss Not Included in the Production Formula (Non-Formula Loss)

- The loss quantity is not included in the production formula.

- Must be stored separately and must not be mixed with formula loss.

- The company must either:

- Export the loss, or

- Apply for destruction approval. After destruction, tax must be paid based on the condition of the scrap, then the account can be adjusted.

Tax Calculation for Commercially Valuable Loss

In the case where Company A purchases raw materials from BOI-promoted Company B and adjusts raw material accounts monthly via Report-V, if both formula and non-formula losses have commercial value, tax must be paid based on scrap condition.

BOI notifies the Customs Department, which inspects and assesses the duty.

ตัวอย่าง:

- Aluminum scrap: 1,000 kg

- Appraised value: 80 THB/kg

- Import duty rate: 0%

- VAT only applies:

1,000 × 80 × 7% = 5,600 THB

Lost BOI-Approved Documents (After 2–3 Years)

If scrap export and account adjustment rights were transferred to a vendor, but the BOI-approved document (red Garuda stamp) was not used and later lost:

- Can BOI reissue the document?

Yes. The IC can issue a new Report-V, provided that:- The vendor files a police report for lost documents.

- The police report is submitted to the transferring company to request reissuance via IC.

- Can the vendor still adjust accounts after nearly 3 years?

Normally, export declarations and Report-V must be used within 1 year from export or issuance date.

An extension of up to 1 additional year may be granted for valid reasons under BOI Announcement No. P.3/2556.

Special Case: Transfer of Scrap Adjustment Rights

If Company A applied to BOI for scrap adjustment and transferred adjustment rights to Company B:

- The transfer document has no serial number or date, making it impossible to verify whether it exceeds the 1-year limit.

- It is therefore understood that Company B may still adjust the account.

- However, if the document is lost, BOI cannot verify whether it was already used, which creates a risk of duplicate usage.

- BOI has no clear guideline for this case; consultation with the BOI project officer is recommended.

Domestic Sale of Scrap Imported Under BOI Privileges

The company may sell scrap domestically, but procedures differ depending on the type of loss:

Formula Loss

- Apply to pay tax based on scrap condition.

- Tax must be fully paid before sale.

- No further account adjustment is required.

Non-Formula Loss

- Apply for destruction approval.

- Destroy scrap according to approved method.

- A BOI-authorized inspector must verify destruction and issue a certificate.

- Apply to pay tax and adjust accounts.

- Tax must be fully paid before sale.

- Submit approval and tax payment documents for account adjustment.

Recycling Scrap

- If recycling occurs within the factory, no BOI approval is required.

- If scrap is sent outside the factory for recycling, BOI approval under Section 36 is required.

Sale Before Tax Payment (Storage Issue)

Selling formula loss scrap before paying tax is not allowed.

If storage space is limited, the company may apply for off-site storage approval under BOI Announcement No. P.3/2556.

Export of Formula Loss Scrap

- BOI approval is required prior to export.

- Upon export, tax obligations for the imported raw materials are released.

- Export procedures should be coordinated directly with Customs.

Repeated Destruction Approval

- If the same type of scrap is destroyed using the same approved method, no new destruction approval is required.

- Quantity stated in the original approval is for reference only.

- Destruction must comply with Revenue Department Order No. P.79/2541 and other relevant regulations.

Finished Goods That Cannot Be Sold

- Finished goods that cannot be sold are considered non-formula loss.

- Must apply for destruction approval.

- Destruction must be inspected and certified.

- The inspector’s certificate is used to adjust raw material accounts.

Important Clarifications

- Formula loss must be stored separately from non-formula loss.

- Formula loss does not require destruction or inspector verification.

- Non-formula loss requires inspection, destruction, and account adjustment.

Approved Destruction Methods

Methods depend on scrap type, such as:

- Cutting, crushing, shredding, melting

- Incineration or outsourcing to licensed disposal companies

Spray painting defective metal parts does not qualify as destruction.

Plastic and Mixed Materials

- Incineration and landfill may be approved depending on material type.

- If scrap can potentially be recycled, BOI may require physical destruction and tax payment instead.

- Additional approval may be required if existing destruction methods do not cover all scrap types.

Non-Formula Loss Definition Example

Loss that occurs irregularly and unpredictably (e.g., bubbles during glue coating) is classified as non-formula loss and must follow the destruction/export/donation procedures.

Timeline for First-Time Destruction

- BOI approval: ~3–4 weeks

- Inspection, destruction, tax payment, and adjustment: total ~3 months

- Frequency can be adjusted based on storage capacity and urgency