Companies operating under the privileges of the สำนักงานคณะกรรมการส่งเสริมการลงทุน (BOI) must carefully manage production scrap and waste materials. Improper scrap handling can lead to compliance issues, tax reassessment, or even suspension of BOI privileges.

Many factories unintentionally create risks due to weak documentation, poor traceability, or misunderstanding BOI requirements.

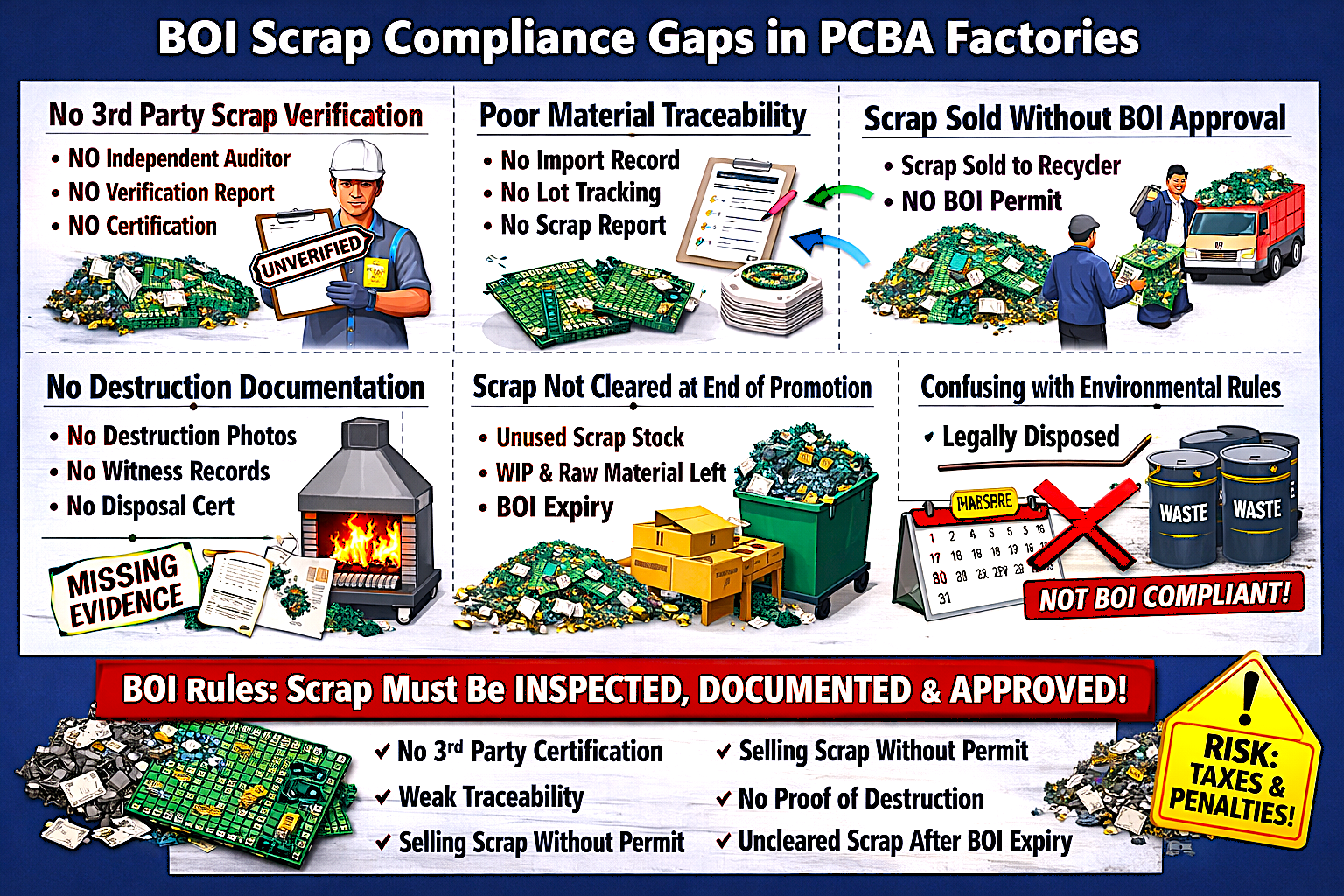

1. No Independent Verification

Some factories record scrap internally but do not use an independent inspection body.

However, BOI typically requires:

- Verification by an independent inspector

- Witness of the scrap destruction process

- Official certification for stock write-off

Without proper verification, companies may face BOI investigation or retroactive tax assessment.

2. Lack of Traceability Between BOI Raw Materials and Scrap

Factories sometimes fail to clearly link:

- BOI imported raw materials

- Work-in-process material

- Generated scrap

Common issues include:

- Missing Material Balance Reports

- Unclear lot tracking systems

This can lead BOI to suspect that raw materials were used for unintended purposes.

3. Selling Scrap Without BOI Approval

A common mistake is selling scrap to recyclers without notifying BOI.

Proper procedure usually requires:

- Declaring scrap quantities

- Allowing inspection or verification

- Receiving approval before disposal or sale

Failure to follow this process may violate BOI regulations.

4. No Evidence of Scrap Destruction

Some factories destroy or dispose of scrap but fail to keep proper documentation.

Required evidence may include:

- Photographic records

- Witness reports

- Destruction records

- Scrap quantity reports

Without evidence, authorities may question whether the scrap was actually destroyed.

5. Failure to Close Accounts When Privileges Expire

When BOI privileges end, companies must reconcile:

- Remaining raw materials

- Work-in-process materials

- Production scrap

If this is not properly reported, authorities may conduct retroactive tax assessments.