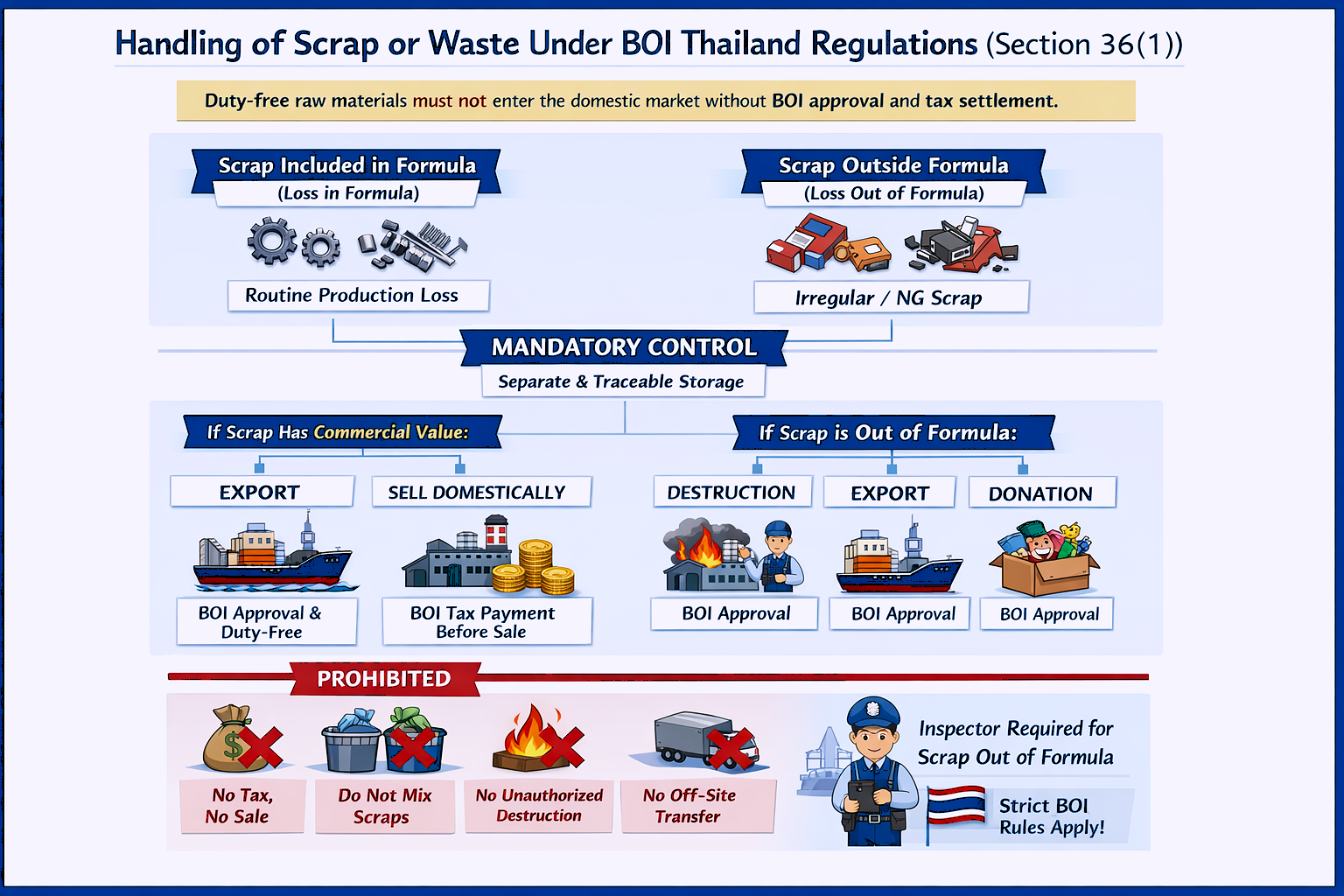

(According to BOI Thailand – Section 36(1))

Under BOI Thailand regulations, scrap, waste, or production loss generated from raw materials imported under Section 36(1) (duty exemption) cannot be handled freely. The handling method depends strictly on the type of loss and its commercial value

1. First Step: Classify the Scrap Correctly

All production scrap must be classified immediately into one of the following two categories:

1.1 Scrap / Loss Included in the Production Formula

(Loss in Formula)

- Loss quantity is approved and included in the BOI-approved production formula

- Occurs regularly and predictably

- Example:

- Cutting loss

- Machining chips

- Trimming waste

1.2 Scrap / Loss Outside the Production Formula

(Loss out of Formula)

- Loss quantity is not included in the BOI formula

- Occurs irregularly or abnormally

- Examples:

- NG products

- Process defects

- Assembly failure

- Cancelled finished goods

2. Mandatory Physical Control of Scrap

According to BOI rules:

- Scrap must be physically separated by category

- Loss in formula

- Loss out of formula

- Scrap must be traceable by:

- Type of material

- Source process

- Quantity

- Mixing different scrap categories is not allowed

This ensures BOI can verify that duty-free materials are not misused.

3. Handling of Scrap Included in the Production Formula

3.1 Accounting Treatment

- Scrap quantity is automatically written off

- Stock cut occurs together with finished goods export (via export declaration or Report-V)

- No separate BOI stock cut application required

3.2 Physical Handling Options

If the scrap has no commercial value:

- It may be discarded according to factory and environmental laws

If the scrap has commercial value:

- The company must choose one of the following:

Option A: Export the Scrap

- Obtain BOI approval before export

- No import tax or VAT payable

- Import duty obligation is fully discharged

Option B: Sell Scrap Domestically

- Apply to BOI for tax settlement

- Pay tax based on the scrap’s physical condition

- Tax must be paid before sale

- No destruction or inspector required

4. Handling of Scrap Outside the Production Formula

Scrap outside the formula is more strictly regulated because it is not pre-approved in BOI production norms.

4.1 Available Handling Methods (Choose One)

According to BOI Notification No. 5/2543:

- Destruction

- Export

- Donation

4.2 Destruction Method (Most Common)

If destruction is chosen, the company must:

- Request BOI approval for the destruction method

(e.g., crushing, cutting, melting, incineration) - Use a BOI-appointed inspector to:

- Verify scrap type and quantity

- Supervise destruction

- Issue a destruction certificate

- Assess commercial value after destruction

- If valuable → tax must be paid

- If no value → no tax required

- Apply for BOI stock cut

- Submit inspector certificate

- Submit tax receipt (if applicable)

- Sell or dispose of scrap

- Only after tax payment (if required)

4.3 Export or Donation

- Requires prior BOI approval

- Export discharges tax liability

- Donation must follow BOI-approved recipients and conditions

5. Tax Principle Applied by BOI and Customs

BOI and Customs assess tax based on:

“The condition of the scrap at the time of disposal”